November 4, 2024

November 4, 2024Probability Tokenization: A Modern Approach to On-Chain Automatic Prediction Markets

catslovefish.eth Edward Lee

1 Introduction

Forecasting the future has forever captivated the human mind, whether it was through ancient oracle bones or by following modern political polling. Whenever we need to plan — be it crops, corporate strategies, or crucial investments — we want the best possible peek at what lies ahead. Economists discovered that certain market mechanisms can gather diverse perspectives and synthesize them into surprisingly effective forecasts. In today’s blockchain era, these ideas have found a new life: open, permissionless prediction markets where anyone can stake their opinion.

Still, most existing on-chain prediction markets mimic either traditional limit order books (which depend on active matching by market makers). Such approaches often require a separate and sometimes cumbersome settlement process: once an event’s outcome is known, protocols must carefully match the winning tokens to collateral and declare others worthless.

This article proposes a simpler, more composable framework called probability tokenization. Rather than splitting outcomes in complicated ways, we issue a distinct ERC-20 token for each possible outcome, tying all outcomes to a single collateral reserve. The magic lies in always minting or burning complete sets of these outcome tokens for exactly 1 USD each. That choice keeps the sum of all outcome prices at $1, a perfect mirror to “probabilities.” Whichever outcome ultimately happens later can be redeemed at $1 per token, while the others naturally fade to zero. Below, we explore how this mechanism works, how it integrates with external trading platforms, how it compares to other approaches, and what key questions remain as the concept evolves.

2 Core Mechanism: Minting All Outcomes at Once

2.1 A Function f : RN →R

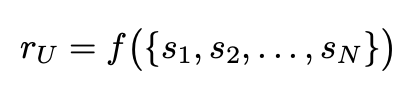

To anchor the idea mathematically, consider N possible outcomes for an event. Let s_i be the supply of tokens for outcome i, and let r_U be the total USD (or stablecoin) reserve. We define a mapping

that links the collective token supplies to the required collateral. We also have the inverse

However, our specific design sets s_1 = s_2 = ···= s_N = r_U , meaning each outcome token supply always equals the entire reserve. Symbolically,

If the contract holds 100 USD in collateral, it issues exactly 100 tokens for each outcome. This makes final settlement direct: once the outcome is known, each winning token is worth $1, with all other outcomes worth $0.

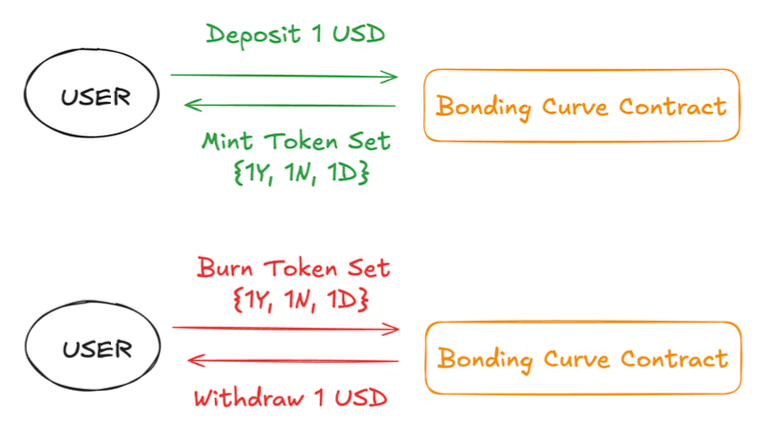

2.2 Illustrative Example of the Mint-and-Burn Rule

Suppose there’s an event with three outcomes: Yes (Y ), No (N ), and Draw (D). When you deposit 1 USD into the protocol, you mint {1 Y , 1 N , 1 D}. This raises the reserve from, say, $10 to $11, and also increases the supply of each token from 10 to 11. Conversely, if you want to withdraw 1 USD, you must return a complete set of {1 Y , 1 N , 1 D}, which then burns those tokens and hands you back $1.

Figure 1: Mint a complete set of outcome tokens for 1. The token supply of each outcome always matches the reserve.

If “Yes” wins in the end, s_Y equals r_U , so every Y token can be redeemed for $1. There is no fractional reallocation or leftover math needed. Tokens for other outcomes simply become worthless.

2.3 Price–Probability Duality

Locally, if you imagine just “buying one extra Yes token” in a vacuum, it might appear to cost $1. But in this protocol, you never buy just a single outcome token from the bonding curve; the system always mints or burns a complete set. So from a global standpoint, all outcome tokens collectively sum to $1. If we have N outcomes, then on external markets their relative prices may shift, yet the total must remain $1. This effectively turns each token’s price into a probability. If one outcome is priced at $0.70, the rest split $0.30.

2.4 Seamless Final Settlement

Once an oracle or authorized mechanism declares the real-world result, tokens for the correct outcome can redeem for $1 each from the reserve. Because the winning token’s supply is always r_U , the match is perfect. Other outcomes instantly lose all redemption value, so no complicated distribution is needed.

3 Trading and Liquidity in Practice

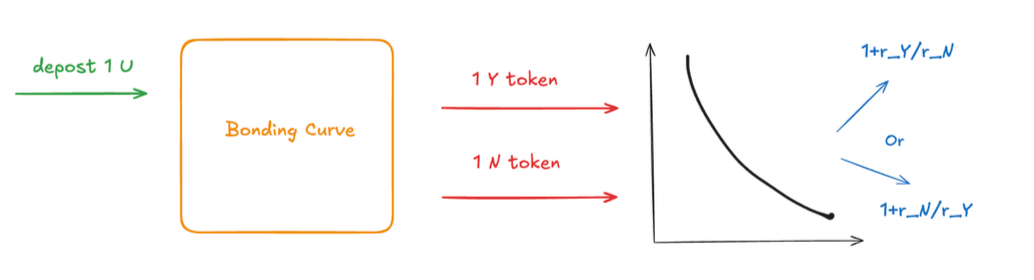

Although the protocol requires a complete set for minting or burning, participants often want to hold only the outcome they believe in. So, after minting, they typically head to an external exchange (such as a Uniswap-style AMM or a centralized platform) to trade away the outcomes they don’t want.

Figure 2: Deposit 1 USD, receive a pair of outcome tokens {Yes, No}, and then trade the one you don’t want. Prices float freely, but their sum stays $1.

For a two-outcome scenario, depositing $1 yields {1 Yes, 1 No}. If you believe strongly in Yes, you can swap your No token for additional Yes on an external market. Over time, the ratio between Yes and No tokens in circulation adjusts as participants continuously trade to reflect new information. Still, the sum of the outcomes in USD remains $1. Because the protocol itself does not differentiate between outcomes, there’s no direct arbitrage inside the mint–burn process. Any potential arbitrage would come from external markets quoting inconsistent prices. The essential role of the protocol is to keep each outcome’s total supply locked to the shared reserve so that final redemption is always fully backed.

4 Comparison with Other Prediction Market Designs

4.1 Traditional Bookmakers

Old-school bookmakers or betting houses set odds and pay winners out of their own pockets. It’s convenient but centralized: the bookmaker might impose unfavorable odds, or fail to pay. By contrast, probability tokenization is trustless, with every token fully collateralized. No single operator sets the price; it’s discovered in the open market.

4.2 Order-Book Based Systems (e.g. Polymarket)

Many on-chain markets, such as Polymarket, rely on central limit order books where participants post bids and asks for each outcome. While this can be powerful, it can become fragmented or illiquid for minor events.

In our approach, anyone can effortlessly create or remove tokens by depositing or withdrawing a complete $1 bundle, ensuring the system never lacks a fallback for liquidity. The actual price discovery occurs on any external exchange where these outcome tokens are traded.

5 Tax, Fees, and Integration with DeFi

5.1 Introducing a Fee

A project could layer in a small tax whenever a user deposits or withdraws $1 from the bonding curve. For example, depositing $1 might cost $1.001 to account for a protocol fee, or withdrawing might return $0.999. This revenue can go to a DAO treasury or fund ongoing development, without disturbing the 1:1 nature of the token/reserve relationship.

5.2 DeFi Composability

Since each outcome token is an ERC-20 asset, it can be plugged into the broader DeFi ecosystem. Traders can add them to Uniswap or other DEX pools, potentially earning fees as a liquidity provider. They could even (if markets accept it) use them as collateral in lending protocols, or stake them in governance systems. This interoperable design is part of what makes on-chain finance so flexible.

6 Open Questions and Future Directions

Although probability tokenization offers a clean, one-stop solution for minting and settling multi-outcome markets, several questions loom for real-world deployments.

Oracle Reliability and Edge Cases. The system hinges on an external oracle correctly identifying the winner. If the oracle is hacked, or if the event is ambiguous or canceled, the tokens could be left in limbo. Designing robust fallback or dispute mechanisms remains crucial.

Burning Winning Tokens and Abandoned Collateral. What if someone destroys winning tokens (sending them to a blackhole address) so that some fraction of the collateral stays locked forever? Should the protocol remain entirely hands-off, or should it allow a forced rescue of orphaned collateral?

Scalability to Complex Outcomes. Our method extends naturally to N possible outcomes. But some real-world events, such as a range of prices, could demand many discrete brackets or a truly continuous payoff. That might lead to a combinatorial explosion in the number of tokens, so more nuanced designs may be needed for large-scale scenarios.

Governance for Upgrades. Even a “simple” system may need updates or patches if vulnerabilities emerge. Balancing decentralization with the capacity to address unforeseen problems is a common challenge in blockchain governance.

Ultimately, probability tokenization attempts to unify the convenience of a single-collateral system with the freedom for external price discovery. As on-chain prediction markets evolve, this model could help expand their adoption, offering a more straightforward path to harnessing collective foresight and making guesses about the future a bit less uncertain.